FHA vs. Conventional Loans: Why These Mortgage Payments Are So Different

When buying a home, one of the biggest surprises for many buyers is how much the type of loan affects the monthly payment. Even when the interest rate is the same, your payment can change dramatically depending on your down payment and loan program.

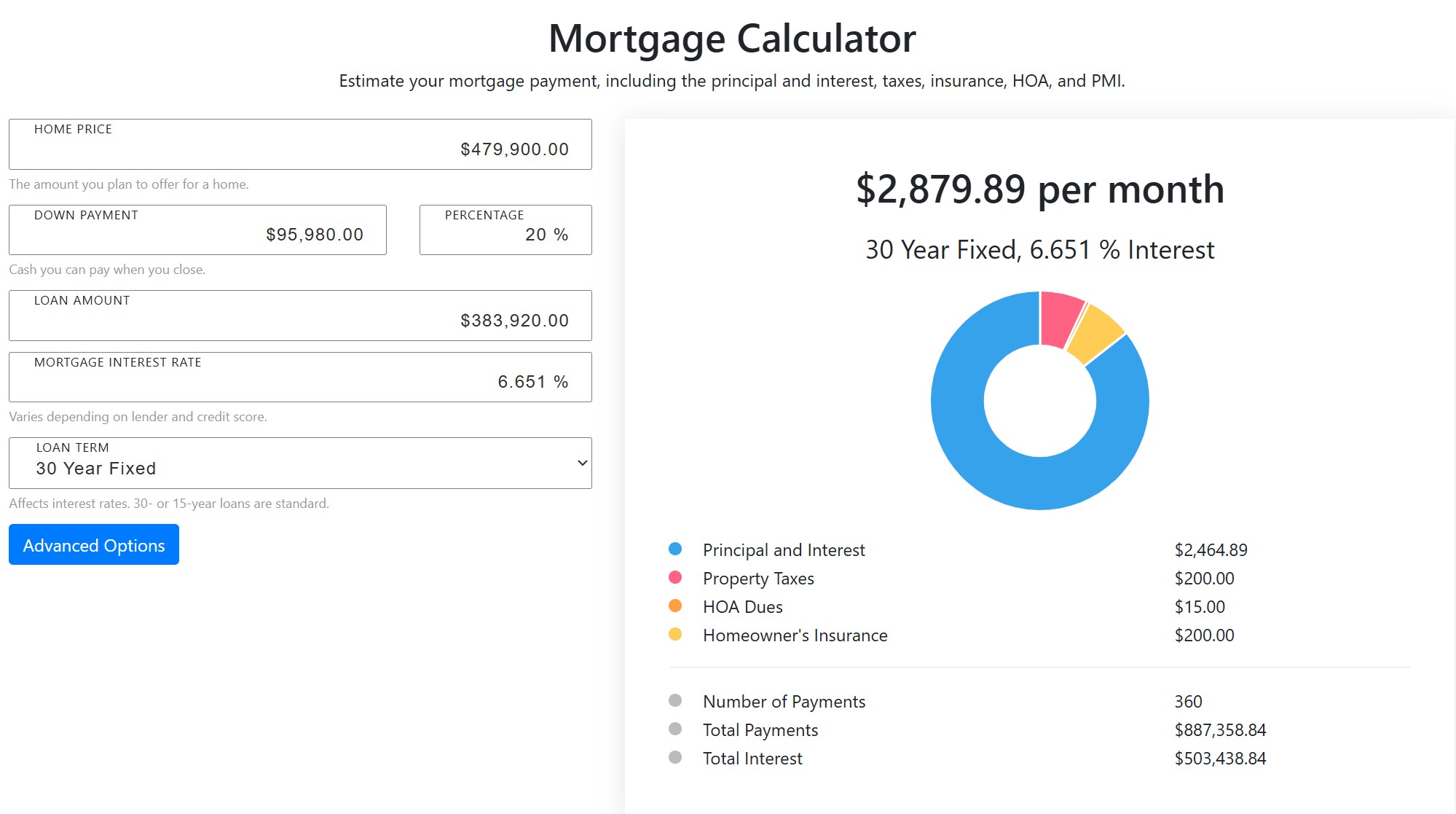

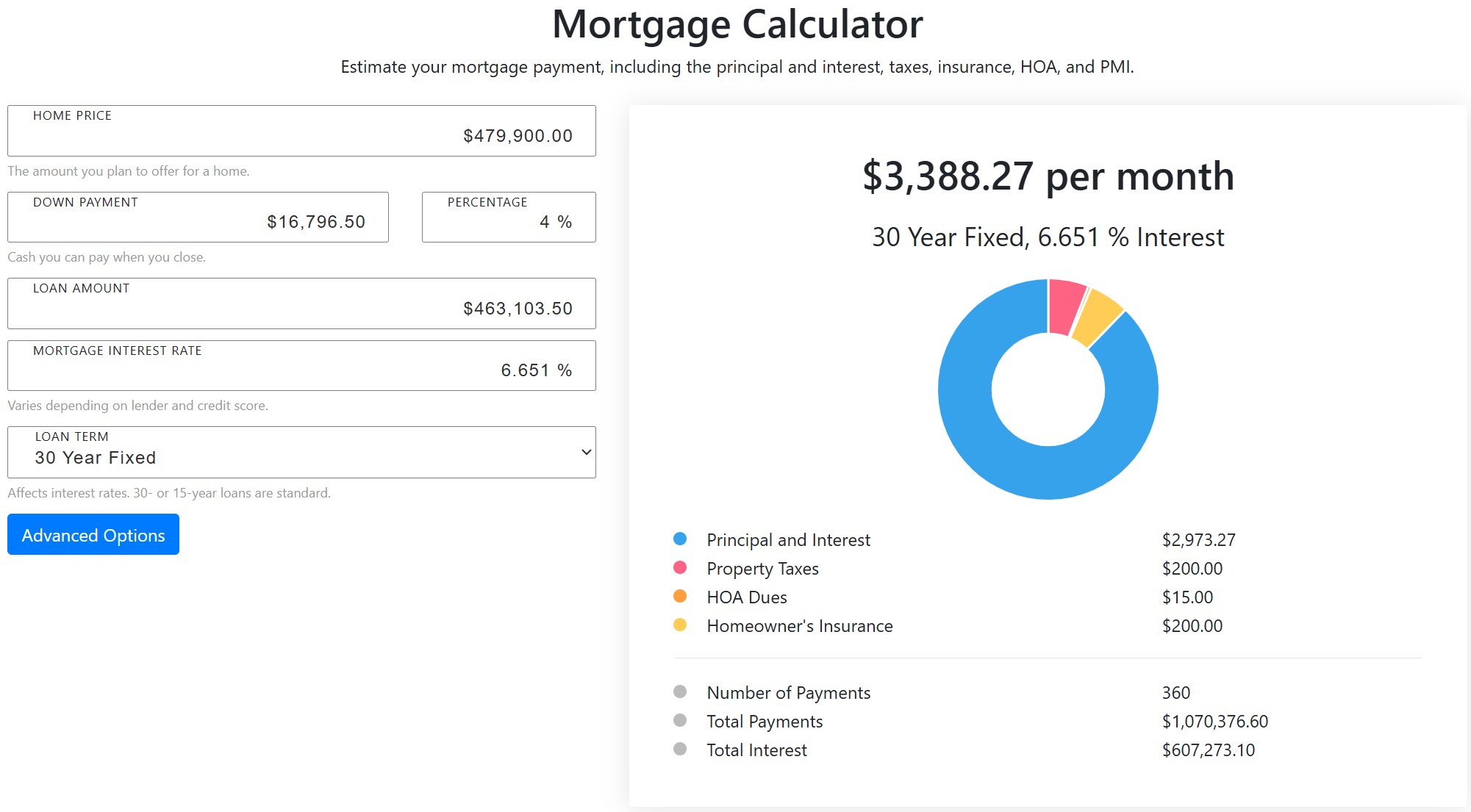

In the examples above, both buyers are purchasing a home priced around $479,900 with the same 6.651% interest rate on a 30-year fixed mortgage. However, the monthly payments are very different because one loan is Conventional financing with 20% down, while the other is an FHA loan with 4% down.

Let’s break down why.

Conventional Loan Payment Example

Home Price

$479,900

Down Payment

20% ($95,980)

Loan Amount

$383,920

Estimated Monthly Payment

About $2,879/month

With a conventional loan, the buyer is putting down a much larger amount upfront. Because of that:

The loan amount is smaller

Monthly principal and interest payments are lower

No monthly mortgage insurance (PMI) is required with 20% down

This creates a lower overall monthly payment and saves a substantial amount of money over time.

Benefits of a Conventional Loan

Lower monthly payment

Less interest paid over the life of the loan

No PMI with 20% down

Often better long-term savings

Things to Consider

Requires a larger down payment

May need stronger credit scores

More cash needed at closing

For buyers who have savings available and want to reduce their monthly housing costs, conventional financing is often a great option.

FHA Loan Payment Example

Home Price

$479,900

Down Payment

4% ($16,796)

Loan Amount

$463,103

Estimated Monthly Payment

About $3,388/month

The FHA loan allows the buyer to purchase the home with significantly less money upfront. That lower down payment can make homeownership more accessible, especially for first-time buyers.

However, there are trade-offs.

Because the buyer is financing a much larger loan amount, the monthly payment increases. FHA loans also include mortgage insurance premiums (MIP), which add to the monthly cost.

Why the FHA Payment Is Higher

The FHA payment is higher because:

The buyer borrowed more money

Monthly mortgage insurance is required

More interest is paid over time

In this example, the FHA buyer pays roughly:

$500 more per month

Over $100,000 more in total payments over the life of the loan

That is a significant difference.

Why Buyers Still Choose FHA Loans

Even though the payment is higher, FHA loans remain extremely popular.

Why?

Because many buyers simply do not have 20% saved for a down payment.

An FHA loan can help buyers:

Purchase sooner

Keep more cash in savings

Qualify with lower credit scores

Enter the market before home prices rise further

For many families, the opportunity to own a home now outweighs the higher monthly payment.

Which Loan Is Better?

The answer depends on your financial situation and goals.

A Conventional Loan May Be Better If:

You have a larger down payment saved

You want the lowest monthly payment possible

You have strong credit

You plan to stay in the home long-term

An FHA Loan May Be Better If:

You need a lower down payment option

You are a first-time home buyer

Your credit score is lower

You want to buy sooner rather than later

Neither option is “right” or “wrong.” They simply serve different buyers and different financial situations.

Final Thoughts

The difference between these two mortgage payments highlights an important lesson in real estate: your loan structure matters just as much as the home price.

A larger down payment can dramatically reduce:

Monthly payments

Mortgage insurance costs

Lifetime interest paid

But lower down payment loans like FHA financing can make homeownership possible much sooner for many buyers.

Before choosing a loan, it’s always smart to talk with a trusted lender and compare:

Monthly payment

Cash needed at closing

Mortgage insurance

Long-term costs

Understanding these numbers upfront can help you make the best decision for your future home and budget.

To Search for Homes, See What's Going On In Your Area, or See the Latest Listings CLICK HERE!

Georgia Evans

(615) 542-7880